Dr. Charlie Hall’s appearance at CNGA’s Horticultural Leadership Retreat on Nov. 6, 2020, was sponsored by Tagawa Greenhouse Enterprises. Hall, a professor and the Ellison Chair in International Floriculture in the Department of Horticultural Sciences at Texas A&M University, shared his economic forecast for spring 2021 based on the ever-changing market conditions. He is renowned as an economics expert specializing in the green industry, including innovative management and marketing strategies, financial analysis, and crop outlooks. Here, his presentation is abbreviated and edited to take into account the publishing of it two months after he made it.

Uncertainty Due to COVID-19

There’s a great deal of uncertainty about the economy due to COVID and because of the election. I tried to get the crystal ball that was going to give me perfect clarity about 2021, but as much as I keep polishing that sucker, it’s still a little fuzzy. And, I want to make this point from the outset: any economic forecast is only as good as the data that goes into it, and particularly in 2020, we’ve had a lot of data issues nationally. The Bureau of Labor Statistics and other folks have really struggled to capture a lot of the things that have been going on.

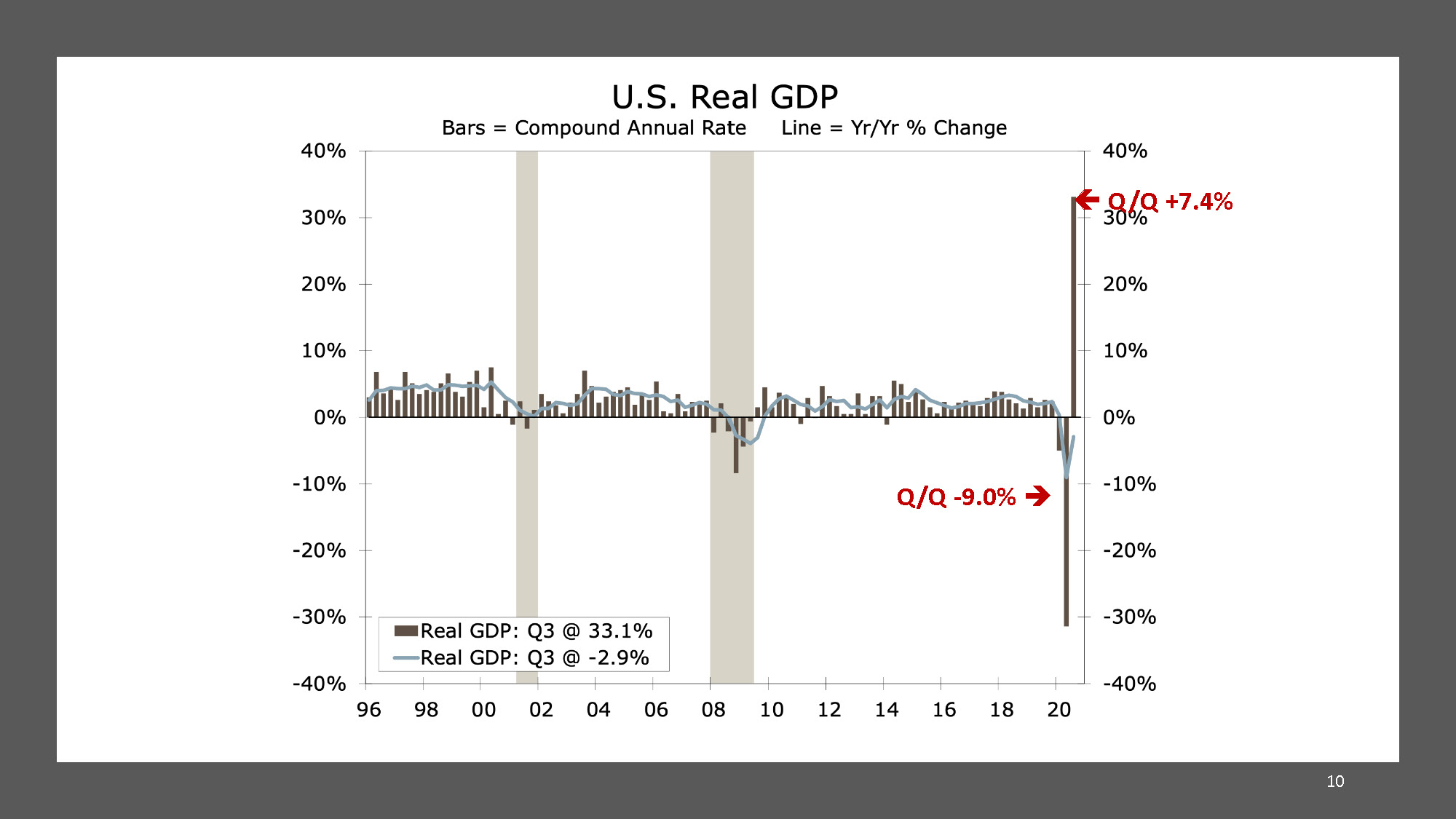

Real Gross Domestic Product (GDP), the leading indicator of the national economy, increased in 2020. But, we are not going to continue seeing that increase. It’s going to slow down pretty dramatically. Consumers are going to keep spending but that too is going to start decreasing. We won’t see those same kind of growth rates.

The good news is that the unemployment policies, including new pandemic-related payments, have been effective in terms of bolstering the consumer. Expenditures rise to meet income. The reason that we have been able to have an increase in our real GDP is that we put money in people’s hands and they spent some of it. People also started saving more. So, we are also seeing the risks ahead of us and we’re starting to save a little bit more, too.

Not all businesses are feeling COVID in the same way. Those that have close contact with customers, like restaurants, bars, clothing stores, food trucks, and gift shops, those have tended to take it on the chin. But those that can distance and safely perform those services without exposure to COVID like landscaping, lawyers, architects, accountants, auto services, roofing, and plumbing, those businesses have benefited.

Dependence on State Policies, Personal Spending and Consumer Satisfaction

In the garden center industry, depending on which state you were in and whether you were deemed essential or not, you either had one of your best years ever or your sales were down. Some of the garden center numbers were anywhere from 10% to 40% up year over year. About three fourths of the nursery and greenhouse growers in the EAGL (Executive Academy for Growth & Leadership) program at Texas A&M were either status quo or up year over year. Then, another 20% to 25% were down because they were located in regions of the country where they weren’t necessarily deemed to be essential.

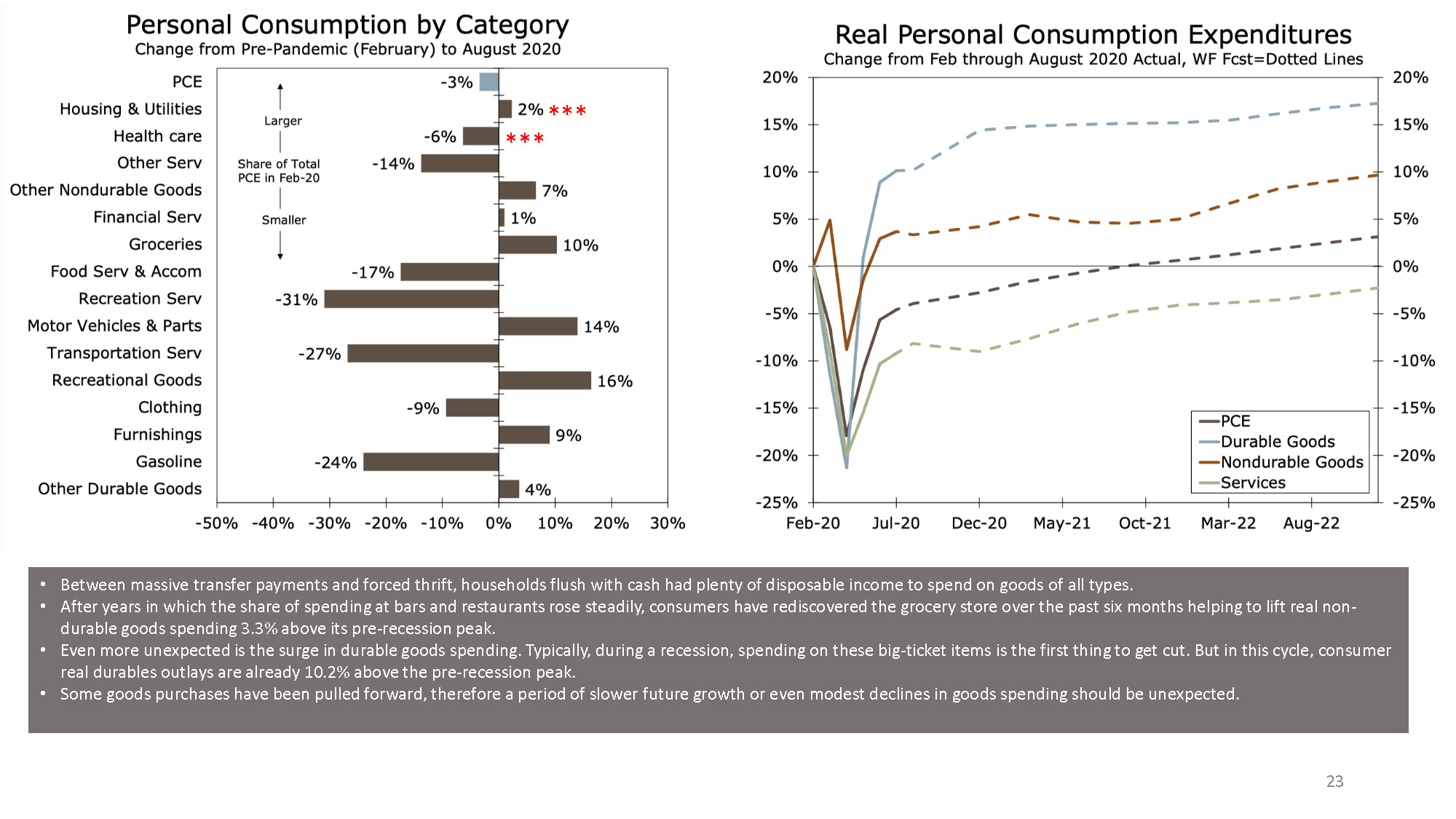

If you look at where we’re spending, this is critical. We’re spending a little bit more on housing and utilities. In the third quarter, people started shifting into purchasing durable goods: cars, furniture, houses, etc. Previously, in past recessions, in the early part of the recession, we wouldn’t have this staycation effect like we saw in 2020 with COVID. People would stay at home more, and 30 years ago, they engaged in America’s number 1 leisure time activity: gardening and landscaping. But, today, gardening and landscaping doesn’t make the top 10 leisure time activity list. Still, in 2020, we saw more people, more newbies in the garden center, buying plants than ever before. The question is: are we going to be able to keep them?

Usually when the economy starts recovering like we’re seeing now, people start switching to buying durable goods. That’s also when they cut back on the green industry. They buy fewer flowers, shrubs and trees. If they’re already making that durable goods switch in late 2020, they may get that out of their systems by this coming spring.

This 2021 season is going to be the litmus test on how well our industry satisfied the end consumer during the pandemic, during the whole staycation effect of COVID. We will see how successful we made them this coming spring. It’s going to be our election, where people vote with their dollars.

I don’t think the shift to durable goods is going to be the headwind that it normally is, so I have a bullish possibility for spring 2021, and I think a lot of it depends on how well we did our jobs in 2020. A lot of businesses, I said, suffered, but for one of the few economic downturns in my lifetime, I’ve seen our industry actually grow during this time period. So, we have been mightily blessed in that regard.

The other thing that makes me somewhat bullish is that if you look at how people spend their money, regardless of our economic conditions, we pay for our healthcare, housing, rent, mortgage, food and beverage, pharmaceuticals, and smartphones. During 2020, the categories with the largest increase in consumer interest were: farms at number one, floral designers, nurseries and gardening, tree services, and landscape architects. Our industry has five categories in the top purchases – that’s pretty good. That makes me pretty bullish.

The other thing that makes me somewhat bullish is that if you look at how people spend their money, regardless of our economic conditions, we pay for our healthcare, housing, rent, mortgage, food and beverage, pharmaceuticals, and smartphones. During 2020, the categories with the largest increase in consumer interest were: farms at number one, floral designers, nurseries and gardening, tree services, and landscape architects. Our industry has five categories in the top purchases – that’s pretty good. That makes me pretty bullish.

The Shape of Recovery and the Role of Preparation

Now, what’s my projection? How do I see this playing out?

It’s based on what is happening with COVID and the nation’s projected shape of the recovery. The economy did not make it back to where we were prior to COVID, when you look at GDP. Our growth rate next year is going to depend on how well we get this health crisis under control. How fast our economy, including employment, personal consumption and residential investment, recovers is dependent on how fast we get on top of COVID. And the growth path from there depends on the pent-up demand (which has been pretty good), the number of business failures, and the policies that are implemented. There’s been several on the Council of Economic Advisors who’ve said we need a CARES Act Part 4 or pandemic relief act part four, and that’s not being done right now, and many believe that policy failure is going to slow down this growth rate by at least 18 months or so. We have got to get something passed in a hurry.

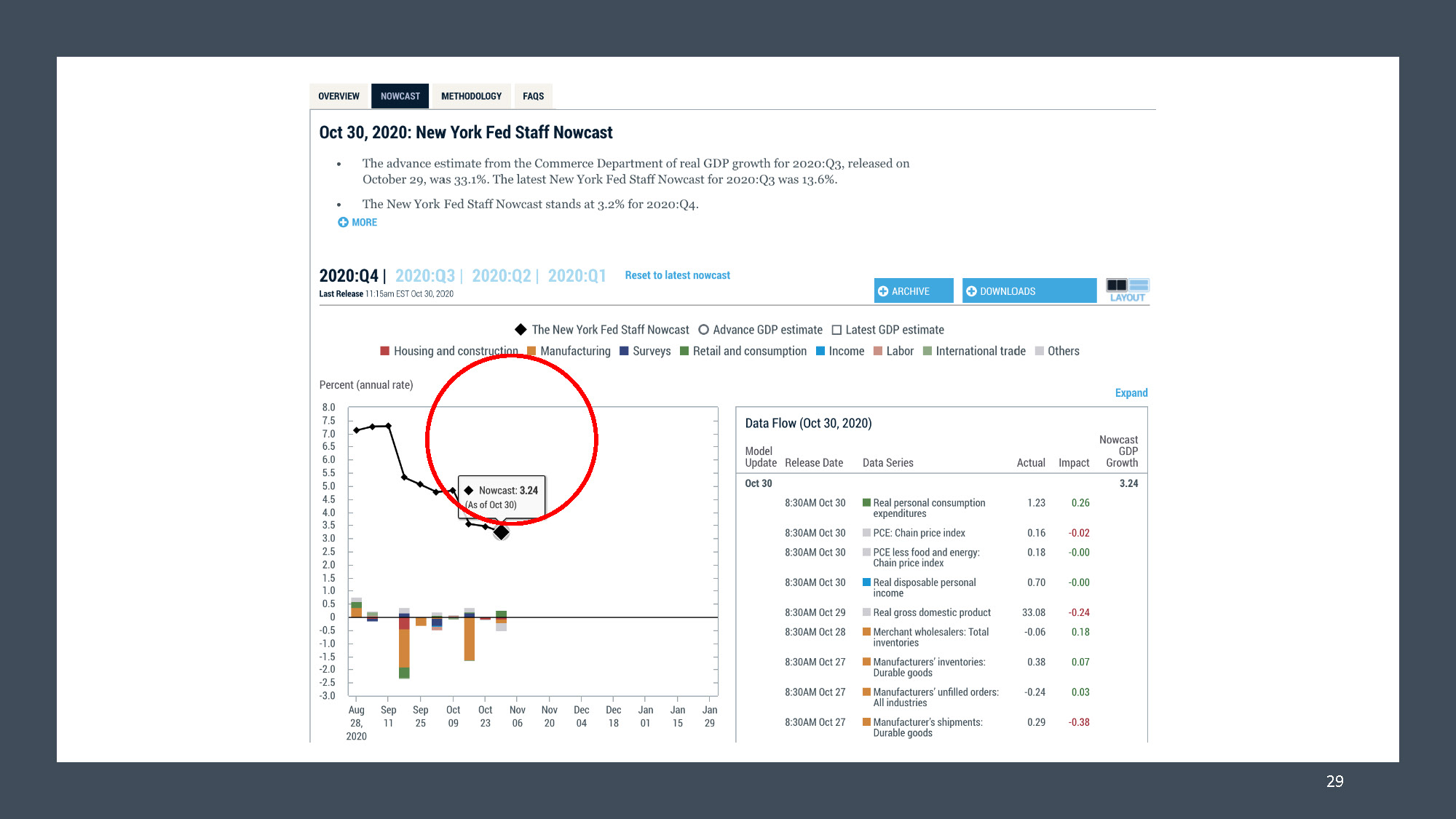

When I look at quarter four of 2020, according to the Atlanta Fed’s GDP “nowcast”, the nation’s projected increase in GDP was 3.4%. Also, the New York Nowcast projected a 3.24% increase for last quarter. So, we were likely to see somewhere in the 3.3% range of annualized growth, but we were still 2.9% below where we were at the end of 2019. Even though we expected to have a really good third quarter and a modestly good fourth quarter, and hopefully the holiday sales were going to reflect that, we’re still down just shy of 3% from where we were at the end of 2019.

When I look at quarter four of 2020, according to the Atlanta Fed’s GDP “nowcast”, the nation’s projected increase in GDP was 3.4%. Also, the New York Nowcast projected a 3.24% increase for last quarter. So, we were likely to see somewhere in the 3.3% range of annualized growth, but we were still 2.9% below where we were at the end of 2019. Even though we expected to have a really good third quarter and a modestly good fourth quarter, and hopefully the holiday sales were going to reflect that, we’re still down just shy of 3% from where we were at the end of 2019.

Turbulent times favor companies that prepare well and take bold steps despite uncertainty. I’ve always said that you do four things during an economic downturn.

First of all, you make sure that you’re operating lean. You should have been doing some lean flow to make sure you’ve got your efficiencies in order.

Then, secondly, you make sure that you are not overleveraged, that the bank doesn’t have more skin in the game than you do. There’s a way to calculate that but make sure you are not overleveraged.

Number three: you manage your working capital. You cut back on capital expenditures, you lay off dead wood in the system (if you’ve got any), and you make adjustments to manage that cashflow (that working capital) in a way that you can manage the downturn.

Then, lastly, you focus on that value proposition. What that means is what value are you offering your customer base that they will deem you to be essential even in the midst of a pandemic, even in the midst of an economic downturn. Do you have a value proposition that resonates with your customer base so that they see you as essential?

If you do those four things, you don’t freak out during a pandemic, and you see the opportunity, then you will see the growth rate. The difference there is between those that anticipate the downturn and build resilience and those that don’t – those that prepare an action plan versus those that are complacent. Those who acknowledge the recession late, they will struggle to grow, but those that see the opportunities and pay attention, they accelerate growth.

Now, what kind of growth rates are we going to have in the spring? In my Your Market Metrics program, we were looking at growth rates and projecting that if I drew a regression line from last spring 2020 sales, the growth rate came to about a 6.5% increase in spring 2021. There are those that are planning on a 20% to 40% increase in the marketplace.

I’m seeing young plant growers having trouble keeping up with the young plant demand. We’re going to go from a situation where garden centers were begging for product even in June 2020, and doing a lot more pre-booking in the fall. That tells me that we’re getting ready to ramp up and go from a shortage situation to a surplus situation. How quickly? Well, in the last 31 years that I’ve been doing this, it’s only taken about a couple of years to get there. So, I don’t know that we’ll bastardize our spring market for 2021. But, I’m sure shaking my head and wondering what kind of situation we’ll have in 2022 and 2023, particularly on the shrub and tree side of things. Because I see a lot of folks planting on the “back 40.” I’m a bit worried about that, but we’ll see how that plays out.

I tell my greenhouse growers, the best sight in the world is when that sucker’s empty because you sold it all versus having to dump some of it. By the way, shrinkage rates and payroll costs went way down last spring. We did more with fewer people and had less shrinkage. There was some product that wouldn’t meet spec necessarily, but it still made it through the supply chain because there was that kind of need.

I’m cautious but you know I’m optimistic. I’ve been referred to as “Professor Silver Lining.” At the same time, I’m going to be very realistic. I’m not going to tell you that we’re going to have 25% growth in 2021, like we had in 2020. I’m going to tell you I would look for a 5% to 10% increase, and if I got 25, all the better.

{kind=link}